So, AMD is the new messiah. I swear, I check my feeds and all I see are rocket ship emojis next to that ticker symbol. The stock has gone from eighty bucks to over $250 since April. Let that sink in. A company that for decades was known as the scrappy, perpetually-second-place alternative to Intel and Nvidia is now being anointed as the next trillion-dollar baby.

And why? Because they finally landed a whale. A big one. OpenAI, the creators of the digital brain that’s currently rewriting half the college essays in America, has decided to buy a mountain of AMD’s new MI450 chips. The market, offcourse, lost its collective mind.

Everyone is screaming about a "re-rating," which is Wall Street's fancy term for "we were wrong before, so now we're panicking in the other direction." AMD’s OpenAI Deal ‘Paves the Way to $300 Price Target,’ Says Analyst. They're calling the OpenAI deal a "masterstroke" that gives the ChatGPT-maker warrants to own up to 10% of AMD. They spin this as a genius move to "financially motivate OpenAI to ensure AMD’s hardware and software are successful."

Let me translate that for you: AMD just gave away a tenth of its future to its biggest new customer in exchange for them agreeing to be a glorified, high-stakes beta tester. This isn't a partnership; it's a golden handcuff. OpenAI is now financially shackled to making AMD's notoriously difficult software ecosystem, ROCm, actually work at scale. What choice do they have?

This Whole Thing Smells Like Desperation

Let's be real. The only reason this deal is happening is because Nvidia has a complete and total stranglehold on the AI market, and they're charging for their chips like they're made of unicorn tears and printer ink. OpenAI, Google, everyone—they're desperate for a viable second option to break the monopoly. They're not choosing AMD because it's the best; they're choosing it because it's there.

And the valuation this desperation has created is just... well, it’s something else. We're talking about a forward price-to-earnings ratio of 110. One hundred and ten times future earnings. The analysts who have to justify this stuff are performing logical gymnastics that would make an Olympian blush. They point to a "PEG ratio" of 1.48 and say, "See? When you factor in the growth, it's actually undervalued!"

This is a bad argument. No, 'bad' doesn't cover it—this is the kind of magical thinking that precedes every market crash in history. You're telling me a company's stock can triple in six months and it's still a bargain? Give me a break. It reminds me of the dot-com era, when people justified buying pet food websites with no revenue because they had "eyeballs." Now it's not eyeballs, it's "projected data center growth." Same game, different buzzword.

The most hilarious part is the official Wall Street consensus. After all this hype, all this breathless coverage, the average analyst rating is a "Moderate Buy" with a price target that's basically where the stock is trading right now. It's the ultimate CYA move. They want the credit if it goes to the moon, but they've given themselves an out if it craters. It ain’t advice; it’s just noise.

The Two Elephants Crammed in This Tiny Room

Amidst all the champagne-popping, nobody wants to talk about the two fundamental, terrifying risks that could bring this whole house of cards down.

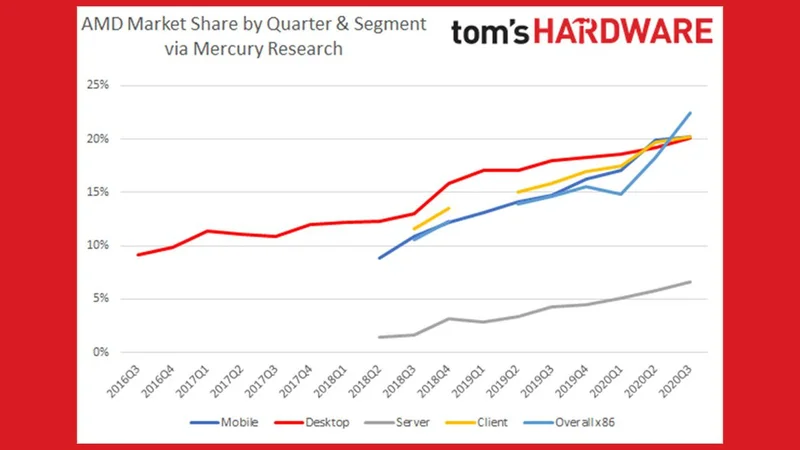

First, the software. Nvidia’s CUDA platform is the iOS of the AI world. It’s a 15-year-old, rock-solid, walled garden where everything just works. You buy the chip, you plug it in, and you go. AMD's ROCm, on the other hand, is the AI equivalent of trying to build a Linux PC from spare parts in your garage. Sure, an army of genius engineers at OpenAI and Microsoft can probably beat it into submission. But what about the thousands of other enterprise companies that want to get into AI? They don't have that army. They want a turnkey solution, not a science project. AMD is selling a monster truck engine; Nvidia is selling a fleet of Ferraris.

The second problem is even more basic: physics. The deal calls for 6 gigawatts of GPUs. Can AMD even get them made? Their manufacturing partner, TSMC, is already running at capacity making chips for Apple, Nvidia, and everyone else. A deal on paper is worthless if you can't get the silicon out of the foundry. It’s a massive supply chain bottleneck that everyone seems content to just ignore, hoping it’ll magically resolve itself. It feels like they're selling tickets to a concert before they've even booked the band or the venue.

Then again, maybe I'm just the crazy one here. Maybe the AI tidal wave is so massive that it will lift all boats, even the ones with a few holes in them. The demand is clearly insatiable, and maybe a slightly janky, hard-to-use alternative is still better than waiting in line for Nvidia's scraps. Maybe this time...

It's a Hell of a Party, But Someone's Gotta Pay the Tab

Look, I get the excitement. I really do. The FOMO is a powerful drug. But buying AMD at these levels isn't an investment; it's a bet at the roulette table. You're not betting on their tech or their long-term strategy. You're betting that the hype will continue long enough for you to find a bigger fool to sell your shares to. The entire bull case rests on the hope that AMD can claw away 10-15% of Nvidia's market. That's not a strategy. That's a prayer. And I stopped praying at the altar of Wall Street a long, long time ago.